A 401(K) is a type of retirement account that allows you to invest in the stock market pre tax and defers that payment until your retirement.

Retirement accounts are miracles in the modern world, They efficiently insured people future by putting money today and investing it all the way until age 60+.

The amount invested called the “principal” is shadowed by the gains on those investments which could be sometimes more than 12 times the amount invested if one starts investing very early in life.

There is potential in every one of us to become millionaires based on this alone, I will explain how in this Post. The question remains ; How quick will we get there ?

The power of compound interest

Like I said earlier the principle is used to invest continuously in different companies through their stocks and then every time there is gains that is added to the total.

That total keeps on growing and every time the higher amount is invested it means more gaines.

It can grow to the point that one year you might be able to make close to one million dollars if the principle is over 10 million. Imagine living off a never diminishing pot of gold!

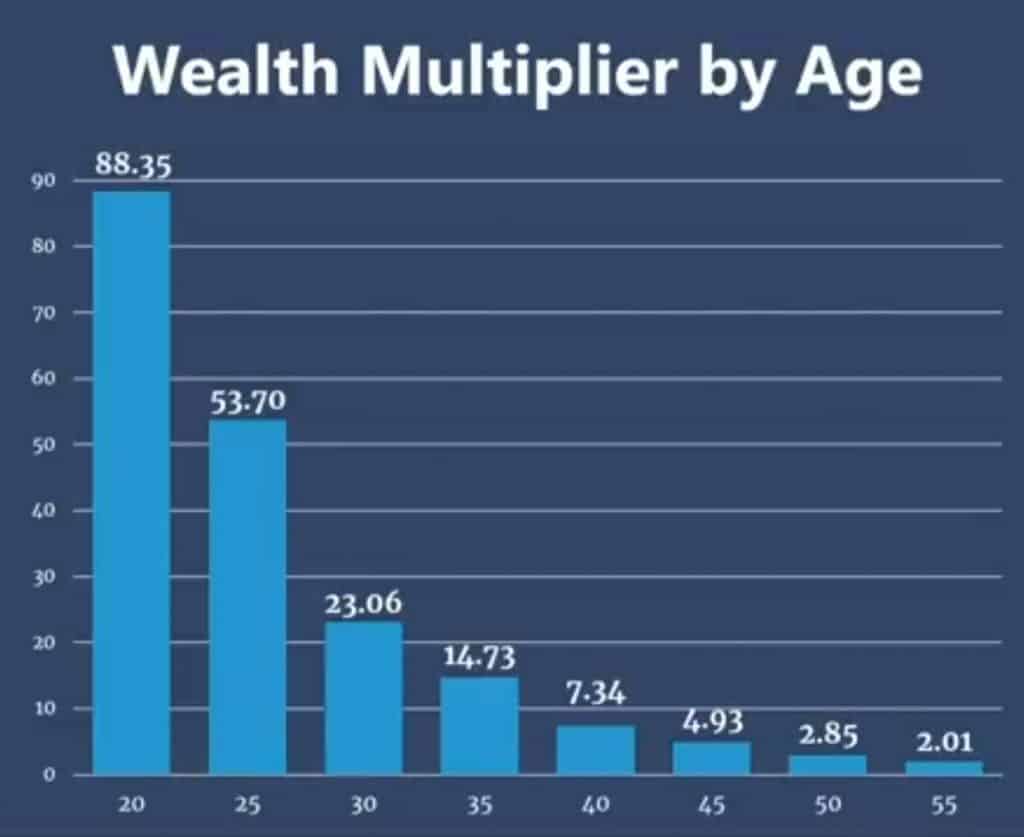

The key to having that great amount for any working class person is to invest as early as possible. For every one dollar you invest at the age 20 equals $88 in retirement.

Take a look at this Graph

To contrast if you invest $1 at age 55 that’s almost equivalent to $2 extra in retirement money so there’s a huge difference to investing early.

Let’s use these hypothetical examples of two investors one is 20 , the other 55+ both contributing $350 a month from themselves and the company matching.

The 20 year old multiplier is 88 for each paycheck : 350 x 88 = $30,800 , $13,200 from the matching per paycheck.

If you’re 55+ then 350 x 2 = $700 , $31.50 from the matching.

How do I invest in a 401(k)?

If you have a job, most companies offer 401(k) plans for their employees. If you are self-employed you can either negotiate opening a 401(k) for your business or you can open a traditional IRA and invest in it.

One main advantage that we have mentioned in the earlier articles is the employee matching programs. Most companies do percentage matching e.g 100% up to 3% and 50% for the next 3% . By this calculation you will have contributed 6%, and your company will have matched that for 4.5% extra so total of 10.5%.

Now some math to put that in perspective , if that 6% equals $200 then the extra 4.5% equals $150 for free for a total $350 for free !

Now, depending on your age, there’s also a multiplier to calculate how much your money will be in retirement.

In our previous example; $13,200 is from company matching in our young investor and $750 is from our elderly investor.

Those examples are on two opposite sides of the spectrum , but both are substantial to illustrate the free money you get from just doing the company matching .

Only other difference is time !

How much should I invest ?

The max for the 401(K) is $19000 in the year 2019 . That equals to $730.76 each paycheck . if you are paid Biweekly. Realistically not everyone can max that out as you need to factor in this money will be taken directly from your paychecks and you cannot withdraw without penalty .

A more practical way is to set a dollar amount e.g our company match example from before of $350 which we will assume is 10.5%

Ideally you would want 15%-20% contributions to retirement accounts . But honestly anything over the company matching would be considered phenomenal .

However, if you want to become a millionaire there is actually very simple math behind that too.

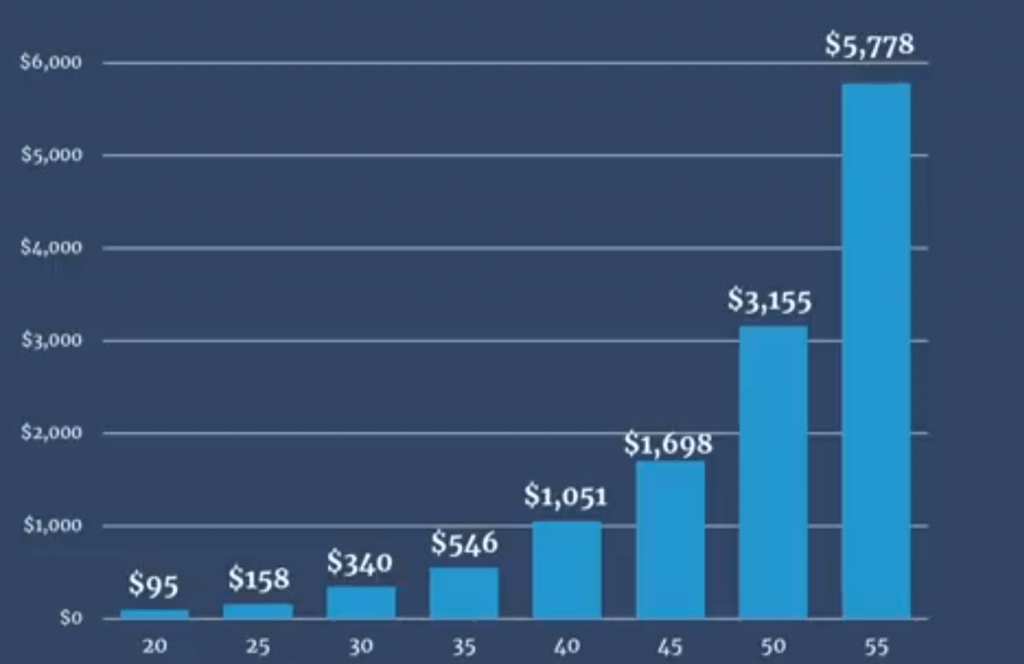

In order to become a millionaire by each age group you have to be saving a certain amount every single month. Take a look at this graph:

Notice again the power of investing early because just by saying saving $95 a paycheck early on you could easily become a millionaire by 65.

But I would consider that the worst case scenario if you’re starting early and investing realistically you want to be able to save as much as you can because the sooner you do that the faster you get to becoming a millionaire.

Personally I save 59.58% of my come every year, and were on track to reaching the goal of having $1.36 Million in 18 years. I have budgeted all of our household expenses and also factor in some major expenses that are not part of the budget.

This allows me to contribute the full amount for my 401(k), Roth IRA, and HSA with a little bit left over every month that I contribute directly to my emergency fund and keep on growing it, or invest even more.

Advance Methods : This is ONLY for People who can Max out the Federal $19,500 Limit

There is a special Trick called 401(K) Front loading that is a great idea . This essentially “Pays your Salary first ” As some entrepreneurs like to say by getting the max employer contribution on as early as possible after the turn of the year .

The basis is that the more time in the market, the more your investments can work for you . So this method unloads all your first paychecks at the beginning of a year until your 401(K) is maxed out – this could take 2-3 months so it is imperative you have a sufficient emergency fund – and then for the rest of the year you will have that army of dollar bills just working for you .

This Tactic allows you to get the full benefit of your employee match very early on in the year and allow that investment to grow the whole year . This is especially valuable if say you had to leave your job during the year and missed out on employer contributions for the rest of the year.

Warning : Some employers have caught on to this tactic and have made the employer contribution on a per paycheck system so always consult with your retirement plan holder .

401(k) or Roth 401(k)?

There’s another type of 401(K) to put your investment in called a Roth 401(k).

Roth 401(k) are essentially the same concept of a Roth IRA, you pay into this account after taxes are paid.

Usually if you’re investing in a 401(k) it is pre-taxed and lowers your total taxable amount per year. For the Roth 401(k) you’re taxed post tax. Your total taxable income is actually higher, and you pay taxes on that amount first.

Afterwards just like a Roth IRA it grows tax-free, and in retirement after age 59 and a half you can withdraw tax free .

When comparing the benefits of one versus the other it is always mentioned that a Roth vessel is good if you know you’re going to have a less income bracket during retirement.

That being said, what if you had a business during retirement? That would increase your taxable income because it puts you in a higher bracket.

Our recommendation is to diversify into both if you intend to have a side business during retirement. For those who do not want to open a business, putting it all into a 401(k) and living in a lower tax bracket during retirement is probably the best choice.

Which stocks do i pick ?

All jobs offer some specific plans, most of which are target retirement plans. You’ve probably seen something like Vanguard target retirement 2050 plan . If you want to be super lazy , this is the choice for you.

If you want to be semi-lazy, and you have the choice available to you, the best recommendations so far is to put all of your stocks portfolio into a total index market fund for example Vanguard VTSAX , or Fidelity’s fund FZROX .

These kinds of funds invest in the S&P 500 top companies. These multibillion dollar companies are also spread internationally too so some consider this a diversified portfolio.

These two plans are essentially investing in the US economy which historically has been performing exceptionally well when you compare it to the rest of the world.

Warren Buffett has mentioned this in his 2018 shareholder letters and saying that investing in one of these index funds is essentially investing in America’s future

If you like to pick individual stocks, a dividend portfolio is a more riskier but very enjoyable and worthwhile endeavor especially if you can continuously work on it for up to 10 years . This is Warren Buffett’s favorite strategy.

A word of caution when investing in individual stocks; try not to run after initial public offering or IPOs . Chances that you’re going to pick the one company that becomes the next Amazon or Microsoft are extremely slim. Even Uber which had an IPO earlier this year has dropped significantly in its valuation.

The reason these companies drop significantly after going public is because they had been living off of Big investors “angel investors “ who covered for their every needs. That does not mean these companies were actually profitable and making money.

Always do your due diligence and study the fundamentals ,balance sheet, business model and the leadership of the CEO. I will Deep dive into individual stocks in an article in the future.

Employee Stock Purchase Plan (ESPP)

This a specific Type of Employer Benefit that is and incentive stock options, they can make it possible for you to buy stock of your employer at a bargain price without reporting income until you sell the stock.

The Qualified ESPP stock Price can be as low as %15 of the price of the stock at the time of Purchase , and an annual investment cap of $25,000 , This is usually NOT done in a 401(K) .

This is immediately a %15 gain on the investment compared to regular market price .

While Not the most tax efficient way but you should buy the maximum you can under your company plan and sell immediately. You’ll pay short term cap gains but it’s free money. You are already heavily exposed to your company by working there so no need to own the stock .

If you’re in a Fortune 500 company that is well off peak and trading at a discount , then you are leaving money on the table if you sell immediately. Make a measured investment decision on whether to hold or sell. Don’t just sell blindly, especially in a dip.

Always do your due diligence and consult your CPA for tax information .

What does retirement look like with this plan ?

For both of the previous investors examples; if you continuously invest $350 a month up to the age of 65 at a 7% Return .The age 20 investor portfolio grew to $$1,327,408.14 and the age 55 grew to $60,579.68

These numbers might be enough for the 20 year old investor as time is on their side. But I highly doubt a 55 year old can survive this. This calculation assumes you are investing with Stocks and not diversified with Bonds.

But don’t worry, there are catch-up mechanisms that elderly can use to increase their retirement contributions and be able to make up for some of the lost time.

For 401(k) and other employee plans, you can put in an additional $6,000 in 2019. For IRAs, you can put in an additional $1,000 if you are above the age of 50.

Ideally, the closer you get towards retirement, the more contributions you need to meet to maximize your retirement, and the more you should contribute to Bonds to protect against Volatility.

So for our 20 year old , even going super aggressive with 100% Stocks would be possible as they have 45 years to recover . While the 55+ should have a diversified 70% and 30% in fixed income bonds .

New IRS Changes for 2020

The IRS just on November 6th 2019 Has announced that all contribution limits for virtually all retirement accounts have been increased ! This is great news . Here are the highlights of changes :

- contribution limit for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan is increased from $19,000 to $19,500

- catch-up contribution limit for employees aged 50 and higher increased from $6,000 to $6,500

- limitation regarding SIMPLE retirement accounts for 2020 is increased to $13,500, up from $13,000 for 2019

- Income ranges for determining eligibility to make contributions to traditional IRAs by $1000 , Roth IRAs by $2000 , and to claim the Saver’s Credit all increased for 2020 by $1000.

- The limit on annual contributions to an IRA remains unchanged at $6,000

Aside from the last point of not increasing Roth IRA maximum contribution limits , all the other changes are for the positive .

Thanks for reading ! Consider reading more articles here.